The most valuable on-the-job experience Dale Heimowitz ever received had nothing to do with his career, but everything to do with money. A few years back, Heimowitz, a 32-year-old who lives in New York City, was working a temp job in the financial sector. He didn’t know anything about the financial world, but for the first time in his life, he found himself surrounded by people who didn’t struggle with money. Heimowitz felt like a fish out of water. “I was just an hourly temp,” he says. “They all got paid real salaries. They had lunch out every day, expensive lattes once or twice a day and fancy dinners all the time. I was just struggling to get by, even with my comparatively cheap rent in Queens.”

The comparison proved inspiring: He decided to learn more about personal finance—something he didn’t learn growing up.

In fact, Heimowitz resisted those fancy dinners and lattes by thinking of his own childhood. Heimowitz’s parents lived in a large house in the suburbs and spent freely. They took on the care of relatives in need. Eventually, however, the costs became too much; Heimowitz’s parents almost lost their home due to compounding financial burdens. The memory of that difficult time keeps him committed to what he’s learned about personal finance: living on a budget and working to pay off his student loans.

And by any measure, he’s working hard. Even in New York City, where side hustles often seem like the norm, Heimowitz’s schedule is head-spinning. He now holds a full-time job as an administrator at a private high school and is a prep cook at a restaurant in the evenings. On weekends, you’ll find him working as a bouncer at a bar.

But extra work hasn’t necessarily meant money in Heimowitz’s pocket. The income from his second and third jobs moved him into a higher tax bracket, which triggered an increase in his monthly student loan payments. His payments doubled, although his income hasn’t, making paying all of his bills more a struggle.

Today, Heimowitz doesn’t even know whether to consider himself working class or middle class. On one hand, he says, his income places him definitively in the middle class. On the other hand, he’s still living paycheck to paycheck, without being able to save anything.

Still, there are things he’s been able to do to stay on top of his student loans and stop credit card debt from compounding. “If I know that one of my credit card bills is becoming a problem, I’ll do a balance transfer to a card with a lower interest rate—or one with no APR for the first year. That helps me pay it down without paying so much in interest,” he says. “I also consolidated my student loans. But I wish I’d been taught about these things earlier on; I would’ve been able to make very different choices.”

Heimowitz feels lucky to have gleaned some knowledge about money through his short stint in the financial industry. But it frustrates him to see his peers struggling to make sense of their own finances. Friends often seek him out for advice about how to deal with a poor credit score, he says, or about how to start a long-term savings plan. Heimowitz sees these questions as a sign that many people his age were never taught about money or investing—and they don’t know where to start.

He can empathize: “I wish I’d been taught early on how to use financial systems to your advantage,” he says. “I remember learning in school that rent is supposed to be no more than a quarter of your living expenses, and that you should be saving 10% of your paycheck. But these guidelines are not realistic when you're working class and in debt.”

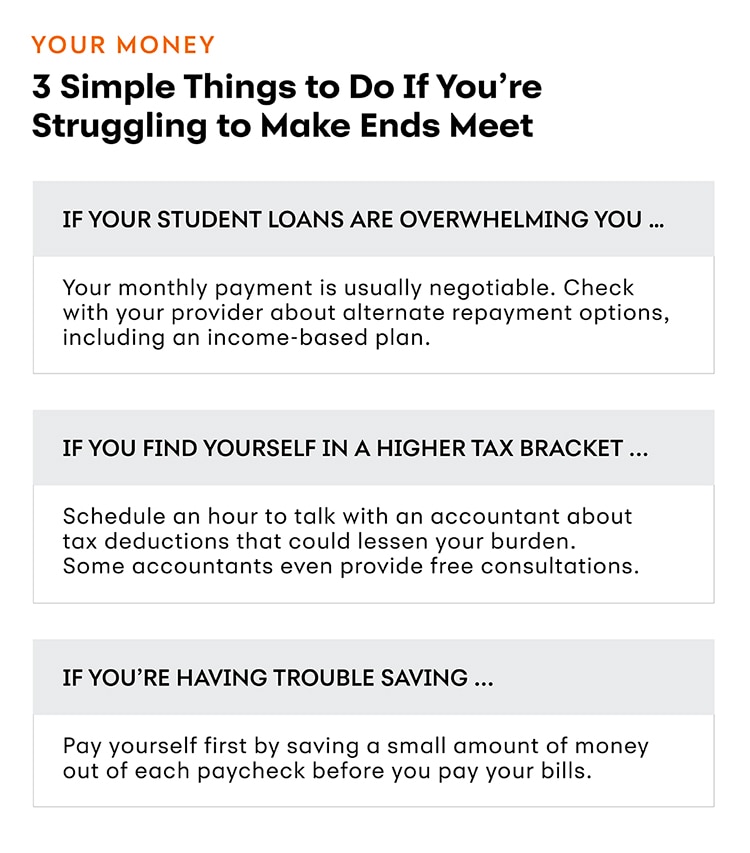

This chart is in the category "Your Money" and is titled "3 Simple Things To Do if You’re Struggling to Make Ends Meet." Number one is if your student loans are overwhelming you. Your monthly payment is usually negotiable. Check with your provider about alternate repayment options, including an income-based plan. Number two is if you find yourself in a higher tax bracket. Schedule an hour to talk with an accountant about tax deductions that could lessen your burden. Some accountants even provide free consultations. Number three is if you’re having trouble saving. Pay yourself first by saving a small amount of money out of each paycheck before you pay your bills.

Donna Sellinger is a writer and educator living in Philadelphia. She loves spending time exploring the city’s parks, museums and riverfront.

Gain confidence in managing your money with our Personal Finance 101 series.