During NCAA March Madness, while my oldest son and I watched 14-seeded Abilene Christian University take down a top seed, I started Googling ACU and other Texas colleges’ tuition costs. My son is 12, so we have a few more years to save, but a glance at those numbers for the state’s public universities and various private schools prompted me to check the balance in our 529 college savings plan—stat.

With three grade-school boys inching toward their teens, once-far-away college costs now loom. Beyond tuition, there are books, housing and other fees, living expenses and, yes, social lives to finance.

My boys will help with part-time jobs and will apply for scholarships, but we can’t count on those. Student loans have their own ramifications, and not everyone qualifies for financial aid. We’re looking to help fund as much of our boys’ education as we can, and it calms my nerves about the “real cost” of college when we research the facts. Here’s some things you may also want to know about college costs in 2021.

What’s the Average Cost for Different Types of Institutions?

Happily, after years of steady increases, the 2020–2021 average cost of higher education dropped approximately 5% in America, for both private and public colleges, according to the U.S. News.

But be wary of thinking that costs will continue on this trend. The pandemic may have prompted the decrease, as many institutions suspended any planned tuition hikes in the wake of remote learning options.

Explore All Your Options

You’re probably aware that public, or “state schools,” typically cost less than private universities, but four-year colleges aren’t the only options. Two-year public colleges, often known as community colleges, can cost significantly less than any type of four-year school, and the pandemic saw a spike in enrollment that typically occurs when economic times are hard, reports CNBC.

Many four-year colleges offer cost-saving 2+2 programs, in which students complete two years at a community college before transferring for the final two years to a four-year school and finish earning their degree. The diploma from the four-year school is the same, but you save money on two years of tuition.

Some students might opt for trade schools, which can teach reliable skills and lead to steady income. My oldest son is good at woodworking, and sometimes I wonder if suggesting trade school to him might be a better route than pursuing a B.S. in IT or going the MBA route. My youngest loves to help in the kitchen and learned to make an omelet by age eight. When he asks if he can crack the eggs, I start thinking about chef school costs. (The Culinary Institute of America has a location in Texas that charges a total of $18,345 per semester. We wouldn’t save much on tuition costs, but perhaps he’ll cook for us in our old age!)

Get Your Students Involved

As they get older, invite your children to help you research costs for all types of institutions. Getting them involved in the process can help them understand what’s at stake. Remind them to check the line items for on-campus and off-campus housing, books, supplies and other fees. Explain the difference between the “sticker price,” which can cause angst, and the net price—the out-of-pocket price you’ll end up paying after you factor in any scholarships and financial aid.

My friend Julie Agan of Atlanta, GA, has a sophomore daughter intent on attending her mother’s alma mater, Auburn University in neighboring Alabama. Agan has warned her daughter that, as big fans of the Auburn Tigers as they both are, she’ll need to earn scholarships to defray out-of-state tuition costs. She’s encouraging her to consider Auburn’s in-state, Southeastern Conference rival, the University of Georgia, which costs a full price of almost $30,000 per year, but offers a net price closer to $16,000.

In Georgia, grade point averages of 3.0 or higher mean high school students can qualify for the HOPE Scholarship, shaving thousands off UGA tuition. Knowing about the HOPE program and that 95% of UGA students receive federal aid in the form of grants, Agan thinks she could get behind the Georgia Bulldogs quickly.

What Does Grad School Cost?

The allure of a grad school degree can keep students happily pursuing their academic dreams or learn valuable, niche career skills. But the cost of two-year graduate programs can soar as high as $100,000 or more, according to U.S. News. For those aspiring to additional higher education—doctorates or professional programs—that could just be the tip of the iceberg.

That’s in part why grad students account for 40% of student loans, which can permanently impact their financial stability. Yes, earnings jump for individuals who received master’s degrees (by about $20,000 per year and more for a doctorate), but those eyeing advanced education should consider the pay scale for the career they plan to pursue after they receive and frame those vaunted degrees.

What Are the Benefits and Risks of Student Loans and Financial Aid?

Student loans serve as a lifeline that allows students the education and opportunity they need, but they can potentially turn into a drag on your student’s financial future. Have a heart-to-heart conversation about what amount of loan your student is willing to shoulder. Is that higher-priced college worth the years of interest it may take to pay for that degree? Or would a degree from a less costly institution mean more financial freedom in the long term? Your family can look at two broad types of student loans:

● Federal student loans: Uncle Sam’s loans have friendlier terms, with lower interest rates and more options if you struggle with repayment. The drawback is that the federal government caps the amount of loans a student can take during their college career at $31,000, according to The Motley Fool.

● Private student loans: If you turn to these, check and double check the terms—including when repayments must start and whether the interest rate is fixed or variable. The last thing you want is for your student to misunderstand the agreement and default on the loan, damaging their credit. And of course, have a heart-to-heart about what amount of loan your student is willing to shoulder. Is that higher-priced college worth the years of interest it may take to pay for that degree? Or would a degree from a less costly institution mean more financial freedom in the long term?

Federal student loans are just one option in the student aid packages that colleges can tailor for students who qualify. Other pieces could include work-study programs, federal grants and aid and grants from the schools themselves. To qualify for any portion of these packages, however, the first step is to fill out the Free Application for Federal Student Aid, affectionately known by college applicants everywhere as FAFSA. Even if you don’t think you’ll qualify for federal aid, the College Board recommends that every student fill it out before the academic year.

How Can I Save Money for College?

Parents typically turn to 529 savings plans, tax-advantaged accounts that allow them to save for future qualified higher education costs by investing in a mix of stock and bond mutual funds. Money can potentially grow federally tax-free, and withdrawals are tax-free for qualified expenses, which now include not only higher education, but also K-12 education costs. Research the best plan available for your situations and remember that 529 plans work best if you start the plan when kids are young and the money you invest has years to grow and compound.

Other common college savings options include the Coverdell Education Savings Account, a trust or custodial account set up to pay for qualified education expenses for a beneficiary—whether it’s your child or a family friend.

You can also save using options such as an IRA, Roth IRA, qualifying U.S. savings bonds, mutual funds and a 529 ABLE plan, but keep in mind that any college savings plans should not interfere with your retirement savings goals. As my financial planner friends have told my husband and me through the years, there are no loans available for retirement, but there are plenty of ways to finance college.

How Can I Cut Down the Cost of College?

Beneath all the strategies for saving, you and your student will need to ask tough questions about how to cut college costs.

● Undergraduate vs. graduate focus: Can a combination of state school for undergraduate school followed by the preferred private grad school lower overall costs and achieve the same career path?

● Starting a 529 Plan early: Can you start saving, either in a 529 Plan or a high yield savings account, when your child is born or under five years old to allow for maximum potential growth?

● Share the burden: Will your child be willing to fill out the FAFSA, research work-study options, seek scholarship opportunities and research alternative degree programs to their top preference?

● Start mentally preparing early: Can you share with middle schoolers, so they understand that, these days, colleges lure students with discounts for good grades? Dubbed “merit aid,” these financial rewards can save you thousands, as much as $100,000 over four years, according to The New York Times.

What’s the Value of a College Degree in 2021?

Occasionally, one of my school-age boys will ask why they even need to go to college. Next time, before I launch into a lecture about how enriching the experience is and how it’s about more than classes, I will simply share what a college degree can be worth in 2021.

According to Georgetown University, that’s $2.8 million on average over a lifetime. And the U.S. Bureau of Labor Statistics notes that holders of bachelor’s degrees have median earnings of $1,173 per week, while those with high school diplomas earn a median of $712 per week.

What Will Your Salary Be After College?

I’m all about following dreams, but I do plan to casually encourage my boys to think about what kind of salary their dreams will translate into one day, when they transform from stars in the sky to coins in their checking account.

For instance, according to January 2021 data from the U.S. Bureau of Labor Statistics, America’s 2 million-plus computer and information technology majors earned a median annual wage of $83,000 in 2018, while a fine arts major, working, say, in graphic design, earned a median annual wage of $40,000. The College Salary Report from PayScale shows that the highest-paying jobs consistently fall in the science, technology and mathematics sectors.

If any of them go the trade school route, salary costs for trade school grads range from a carpenter at $48,330 per year and a plumber at $55,160 per year to a home inspector at $60,710 per year. While these jobs offer consistent income, there’s typically not as much chance for advancement or bonuses and benefits, such as a 401(k) match.

In the End, Help Your Children When They Choose

Wherever our boys end up in school and whatever they study, we’ll figure it all out. But I’m glad we’re thinking about it now, before middle school begins. No matter what age your student, it’s time for you to think about it and plan for it, too.

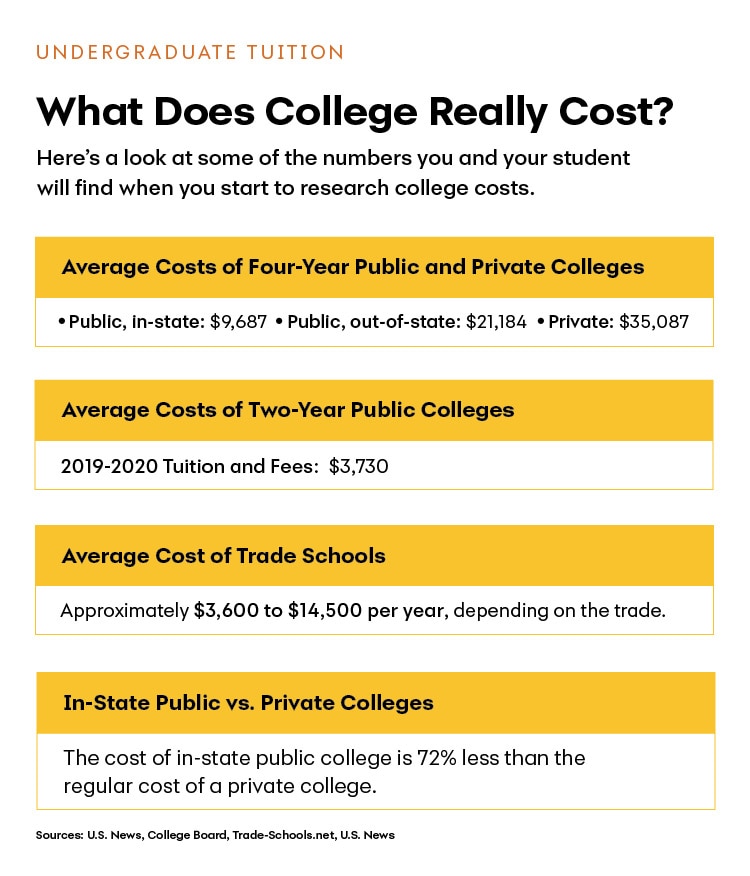

This chart details the costs of specific types of colleges. The chart is titled "What Does College Really Cost?" and is in the category of "Undergraduate Tuition." The introductory text says, "Here’s a look at some of the numbers you and your student will find when you start to research college costs." The first section is "Average Costs of Four-Year Public and Private Colleges" and it shows that public, in-state colleges costs $9,687, public, out-of-state colleges cost $21,184, and private colleges cost $35,087. The second section is "Average Costs of Two-Year Public Colleges," and shows that the 2019-2020 tuition and fees come to $3,730. The third section is "Average Cost of Trade Schools," and shows approximately $3,600 to $14,500 per year, depending on the trade. The final section is "In-State Public vs. Private Colleges" and it says that the cost of in-state public college is 72% less than the regular cost of a private college. Sources for the chart are U.S. News, College Board, Trade-Schools.net, and U.S. News.

A former executive editor at Time Inc. and longtime freelancer, Jennifer Chappell Smith has more than 25 years experience writing about lifestyle, personal finance, and more. She and her husband live in San Antonio, Texas, where they're raising three boys, ages 12, 11 and 9.