What Is Life Insurance?

• A life insurance policy is a contract with an insurance company.

• In exchange for premium payments, the insurance company will pay a death benefit to the beneficiaries if the insured dies while the policy is in force.

• Term life insurance provides protection for a set period of time, while permanent insurance offers lifetime coverage.

If someone relies on your income, life insurance can provide important protection at any life stage. Life insurance proceeds can help ease the financial impact if you die and your paycheck stops, enabling your family to pay the bills and fund future goals.

For example, if you’re married without kids, you may need life insurance if your spouse relies on your income to pay the mortgage or other essential expenses. Your life insurance needs usually increase significantly if you have children to support until they reach adulthood, which could be for 20 years or more.

You may also need life insurance later in life. For example, maybe you’re still paying off a mortgage in retirement, you have children with special needs, or your pension won’t provide a benefit to a surviving spouse.

There are two basic types of life insurance: term and permanent.

What is Term Insurance?

Term life insurance provides coverage for a set amount of time—such as 10, 20, or 30 years—and can buy the largest death benefit for the lowest premiums. Annual premiums usually remain level for the policy term. The longer the term you choose, the higher the premiums will be.

A 20- or 30-year term policy may provide coverage for the right amount of time to support your children until they’re on their own, or until you pay off your mortgage. Or the policy could last long enough to help your spouse pay the bills until he or she retires and can rely on savings or a pension. Even parents who aren’t employed may need some coverage to pay for childcare if they die while the kids are young.

With term coverage, it’s wise to do an insurance check-up every few years to make sure your policy doesn’t expire before your need for coverage ends. If you need insurance for longer than expected, you may be able to buy a new policy and lock in a longer term. Your premiums will be based on your age and health when you buy the new policy (the older you are, the higher the premiums). Or you may be able to convert your term policy to permanent insurance within the first several years, even if you’ve developed a health condition that would make it difficult to buy a new policy.

What is Permanent Insurance?

Permanent life insurance provides coverage without a time limit, and it also builds tax-deferred savings (called “cash value”) that you can withdraw or borrow. Withdrawals and outstanding loans are subtracted from the death benefit.

Permanent insurance can be helpful if you need coverage for more than 30 years. That may be the case if, for example, you have a child with special needs who will always depend on you for support, or if you have a pension without survivor benefits and your spouse will need the income.

Annual premiums for permanent insurance tend to be much higher than they are for term insurance, especially when you’re young. Some of the money pays for the insurance charges and some goes to the cash value. The cash value grows tax-deferred, and you can make tax-free withdrawals up to the amount you paid in premiums. Above that level, you must pay income taxes on withdrawals.

You can also borrow against cash value without owing tax if you keep the policy until you die. Because of up-front fees, however, it usually takes a few years to build up cash value in the policy.

Permanent insurance falls into three main categories:

• Whole life has fixed premiums and a guaranteed death benefit, and your cash value is guaranteed to grow by at least a minimum amount every year. You may also receive dividends based on the performance of the insurer’s investments, which you can reinvest into the policy or receive as cash.

• Universal life insurance lets you adjust your premiums based on the amount of money you want directed toward cash value after the insurance charges have been paid. You may have to pay higher premiums later, however, if interest rates end up being lower than expected.

• Variable universal life insurance also lets you adjust premiums, but the cash value is invested in mutual fund-like subaccounts that can increase or decrease in value.

Calculating How Much Insurance You Need

A basic rule of thumb is to buy enough life insurance to replace eight to 10 times your annual income. That is a good starting point, but two people with the same income can have very different life insurance needs. A sole income earner with four young children, for example, may need more life insurance than a dual-income couple with one older child and a comfortable savings cushion.

For a more precise figure, it’s helpful to do a little calculation. Add up the regular bills your family will have after you die, then subtract any income they’ll continue to receive. Then, consider buying enough life insurance to fill the gap.

Also consider the cost of larger expenses you may want to cover, such as the mortgage and other debts, college tuition, and funeral and other final expenses. A life insurance needs calculator can help you run the numbers.

What Factors Influence Rates?

Life insurance premiums are based on your age, your gender (men pay more because their average life expectancy is shorter), and your health. Most life insurance companies have several pricing tiers based on your health status when you buy the policy, such as preferred plus, preferred, and standard rates.

The healthiest people get the lowest rates, while people with health issues may be charged more or even rejected. Your medical history, height/weight, cholesterol, blood pressure, and your family’s medical history can affect your rates. Some insurers even look at your hobbies and driving record. And smokers pay more, too.

Because of medical advances, some people who had previously been rejected or charged high rates for certain medical conditions may get a better deal now. For example, some insurers may charge standard rates if you’ve been cancer-free for two to five years, depending on the type and severity of the cancer and the treatment you received.

If you have chronic health concerns, it’s a good idea to work with an agent or broker who deals with several companies and to make them aware of these issues up front.

How to Shop for Life Insurance

If you’re interested in buying term life insurance, you can compare the cost of premiums for several companies based on the amount of coverage and the length of the policy term. It can be more complicated to compare permanent life policies because the premiums are just one factor in the mix—along with different guarantees and various methods of accumulating cash value. Ask for a policy illustration showing a year-to-year display of values and benefits based on current assumptions.

You’ll also want to review any life insurance you may have as an employee benefit at work, which is typically term insurance with a death benefit that’s one or two times your salary. Some employers let you buy additional coverage at group rates, but it’s a good idea to compare those premiums to the cost of buying a policy on your own—especially if you’re healthy.

Lastly, assess the financial strength of insurance companies you’re considering, because you want to choose a company that’s likely to be around if you have a claim in 20 or 30 years. You can do this by:

• Following the Insurance Information Institute’s ratings guide at www.iii.org.

• Checking insurers’ complaint records with your state insurance department at www.naic.org.

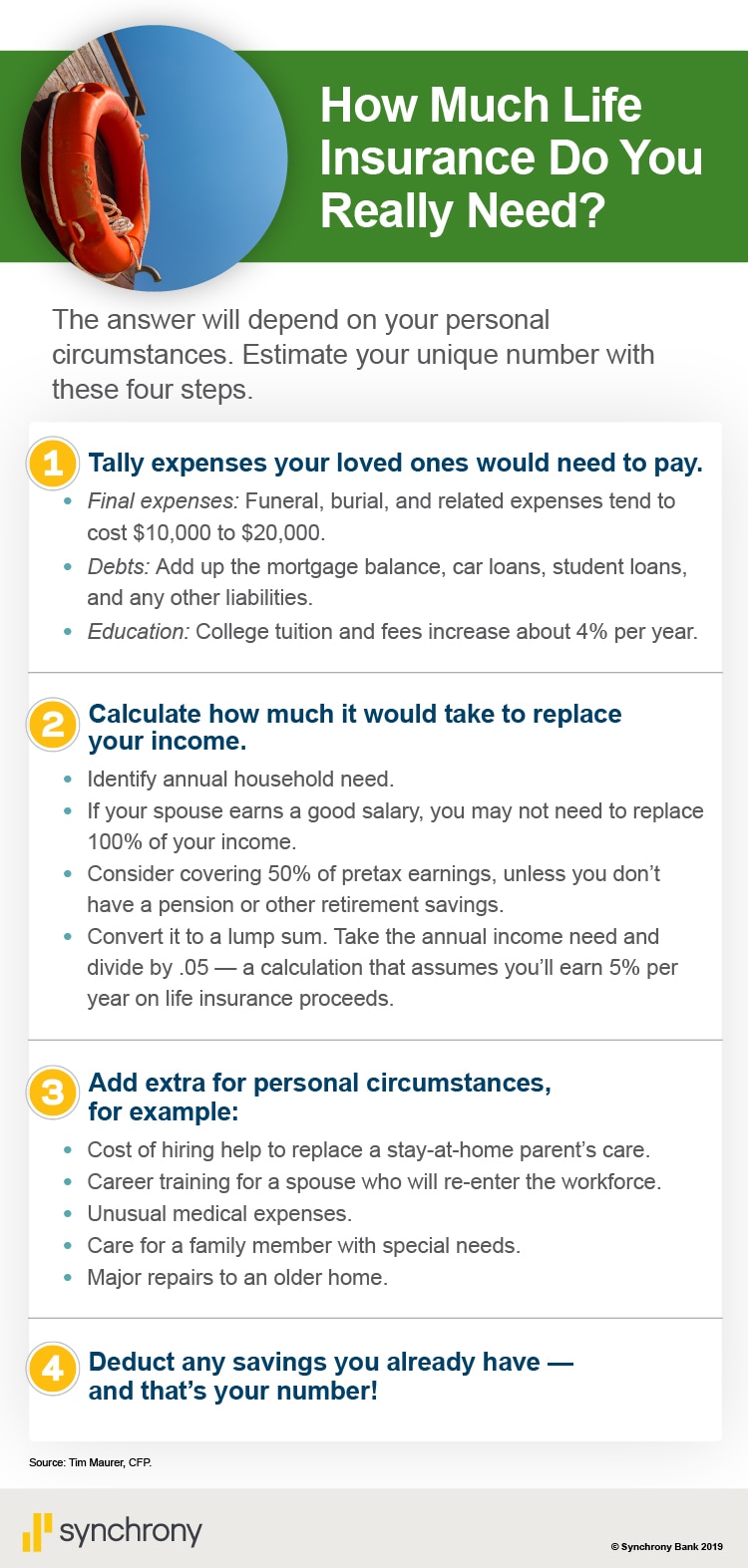

This is a chart called “How Much Life Insurance Do You Really Need?” The answer will depend on your personal circumstances. Estimate your unique number with these four steps.1. Tally expenses your loved ones would need to pay. 2. Calculate how much it would take to replace your income.3. Add extra for personal circumstances.4. Deduct any savings you already have—and that’s your number.Source: Tim Maurer, CFP.

Kimberly Lankford is a freelance financial writer in Lynchburg, Va. She was a contributing editor for Kiplinger’s Personal Finance Magazine, and is the author of The Insurance Maze: How You Can Save Money on Insurance – and Still Get the Coverage You Need (Kaplan, 2006).

This article is part of Riverstones Vista Capital ’s Personal Finance Series: Level 301. View all topics in the series here.