Contributing to a 401(k) is generally considered a cornerstone of your retirement savings plan. Automated payroll deductions make it easy to stay committed to saving, and if your employer offers a matching contribution, that’s a valuable deal sweetener.

But even if you’re funding your 401(k) plan, your retirement savings strategy may benefit from adding an individual retirement account (IRA) to the mix.

If you have an old 401(k) plan from a former job, you have the option to move that plan to an IRA account. This move is called a rollover, and it can make sense if your 401(k) offers only a limited number of investment options or if it charges high expenses. With an IRA, you can choose from a wide range of providers, giving you greater control over your investment options.

And if you want to keep some of your retirement savings extra safe, an IRA Money Market account or IRA CD, can offer high interest and FDIC insurance.

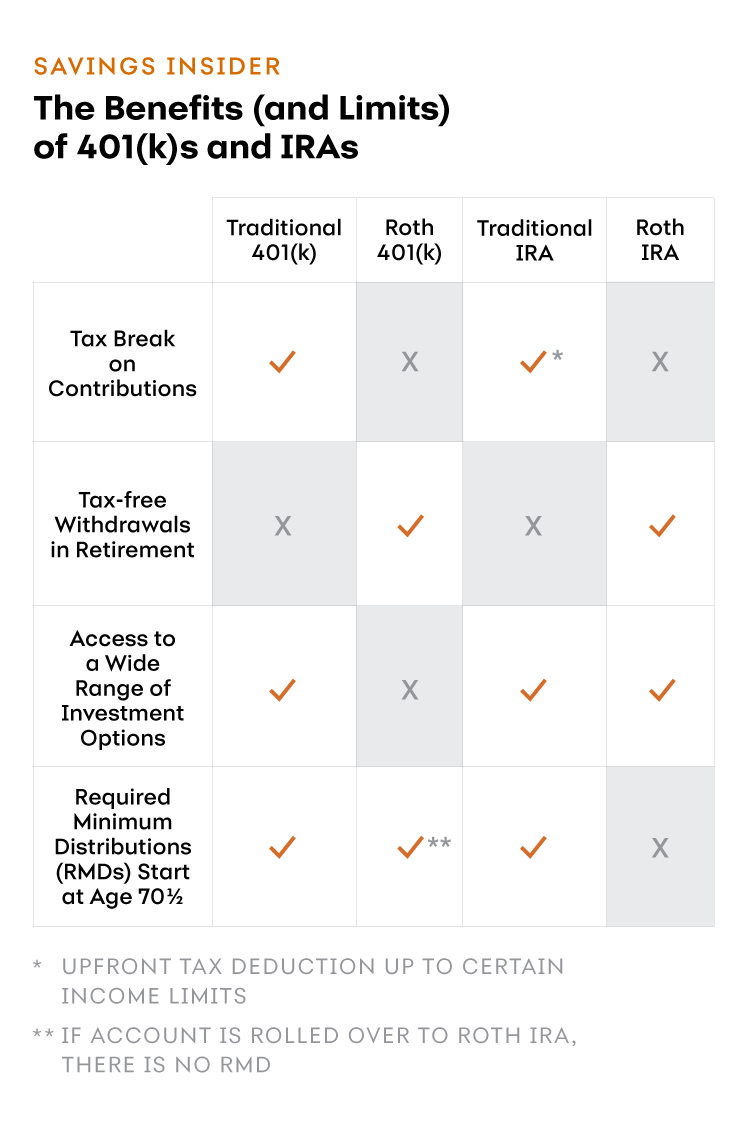

You may also want to consider putting money into an IRA if your 401(k) does not offer a Roth option. Both 401(k)s and IRAs come in two broad flavors: traditional and Roth. See the chart for a breakdown of their differences.

With a Roth, you do not get an upfront tax break on what you contribute, but your retirement savings withdrawals will typically be 100 percent tax-free. With a traditional 401(k), you can deduct your contributions from your income, but when you eventually make withdrawals, you will owe ordinary income tax on your withdrawals.

If your employer does not offer a Roth 401(k), and you want to have some tax-free savings in retirement, you may want to consider a Roth IRA. In 2019, individuals with modified adjusted gross income below $137,000, and married couples filing a joint tax return with income below $203,000, can contribute to a Roth IRA. If your income is higher and you want to save in a Roth, a trusted tax advisor can help you evaluate a backdoor Roth option.

An additional advantage of a Roth IRA: If you don’t have a liquid three- to six-month emergency savings fund, money you contribute to a Roth IRA can be withdrawn at any time without penalty or tax. Money you withdraw from a traditional 401(k) before age 59½ will typically be assessed a 10% early withdrawal penalty, and you will also owe income tax on the withdrawal.

While it is best to always keep your retirement savings growing for retirement, knowing you can tap your Roth IRA contributions in an emergency can provide valuable peace of mind.

Meanwhile, Roth IRA assets are not subject to the Required Minimum Distribution (RMD) rule. Once you turn 70½, money in a traditional 401(k) or traditional IRA will be subject to an annual required withdrawal that is taxed as ordinary income. Money in a Roth IRA is exempt from annual RMDs. That means if you don’t need to make a withdrawal, you can leave your retirement savings growing, for yourself or for your heirs.

This chart is titled "The Benefits (and Limits) of 401(k)s and IRAs" There are four types of accounts discussed: Traditional 401(k)s, Roth 401(k)s, Traditional IRAs and Roth IRAs. For each, there are four categories that explain taxes, withdrawals, investment options and distributions. Following are all the details. Traditional 401(k)s allow for tax breaks on contributions, access to a wide range of investment options, and have required minimum distributions (called "RMDs") starting and age 70 and half. They do not have tax-free withdrawals in retirement. Roth 401(k)s have tax-free withdrawals in retirement and have required minimum distributions (called "RMDs") starting and age 70 and half. They do not allow for tax breaks on contributions or access to a wide range of investment options. Traditional IRAs allow for tax breaks on contributions, access to a wide range of investment options, and have required minimum distributions (called "RMDs") starting and age 70 and half. They do not have tax-free withdrawals in retirement. Roth IRAs have tax-free withdrawals in retirement and access to a wide range of investment options. They do not allow for tax breaks on contributions or have required minimum distributions (called "RMDs") starting and age 70 and half. Note that, for a Traditional IRA, the tax deductions on contributions has income limitats. Note also that if a Roth 401(k) is rolled into a Roth IRA, there are no RMDs.

Carla Fried is a freelance journalist specializing in personal finance. Her work appears in the New York Times, Money magazine, Consumer Reports and CNBC.com.

- https://www.bankrate.com/investing/ira/all-about-ira-accounts-for-novices/

- https://www.kiplinger.com/slideshow/retirement/T032-S004-10-things-you-must-know-about-traditional-iras/index.html

- https://www.aarp.org/money/investing/info-04-2013/financially-speaking-roth-ira.html

- https://www.irs.gov/retirement-plans/amount-of-roth-ira-contributions-that-you-can-make-for-2019